I fact checked the Friendlyjordies vaccine video and it was a bloodbath.

I run a startup that’s building a product to help people capture and share their research processes, archiving source materials as they go. It’s like Twitch but for journalists and other public-facing researchers. A few weeks ago, we released a new BETA version. Part of my job is stress testing the software to see how it stands up to a real world use case. On 21 July, I decided to fact-check a Friendlyjordies video released two days prior, called “Why You’re Not Vaccinated…” which I (a subscriber) had been looking forward to watching, but not had time for yet. A long-term admirer of the channel, I had even approached them in 2019 about an (aborted) plan (which they declined) to have paid guest bloggers use early versions of the software.

My impression at the time, which I had not re-examined until now, was that they were a comedic but factually sound channel. I decided to test this perception by checking this most recent video in a structured and methodical way. The results shocked me.

I identified 15 claims leaving out editorialisations and vague claims such as “Kevin Rudd’s mad” and the government “fucked up” the vaccine roll out. I then located and examined the source materials shown onscreen by FJ and depending how contentious the claim was, looked for confirmation or contradiction of it in other media, then rated it between 0-1, with 0 being a total fabrication and 1 being a totally factual statement. I found seven of the claims to be completely true, three to be more than half true, and five to be less than half true. No claims received a score of 0 – which would mean total fabrication. The average truth score was 0.7.

The most egregious falsehoods (scoring 0.1) are the first two checkable claims. The first of these is that “we have a seven percent rollout”. This had been corrected to 8% in text on screen, to match the source article which was showing on screen. This source article was published by The Guardian on 1 July, and used numbers from (and linked to) a weekly update posted to health.gov.au that same day. In the 17 days between the article and the video being released, there had been two more weekly updates, and 17 daily updates to these numbers (though for some reason none on the day of the video release itself). The most recent update put the number at 13.59, almost double the figure cited by Jordies.

The second checkable claim also scored 0.1 out of a possible 1, as it is another example of an extreme falsehood. The claim was:

“Scott Morrison seems to have brought our entire vaccination supply off of whether it pumps up Dave Sharma’s share portfolio, not if it causes blood clots”

A source for this was an (excellently sourced and extremely specific) article by Michelle Pini in Independent Australia which suggests that two of Dave Sharma’s share purchases should be investigated, as government decisions would later benefit the companies whose shares he had purchased. Another article by Shane Dowling on Kangaroo Court of Australia comes right out and uses the words “insider trading” to describe Sharma’s actions. But neither suggest, as FJ does, that Morrison has factored Sharma’s interests into policy decisions. This appears to be an accusation entirely of FJs confection. In searching for any articles about this, I found an article in the Sydney Morning Herald about conflict between Sharma and Morrison over policies relating to gay teachers in private schools, and another in Junkee, about Morrison getting Sharma’s first name wrong on Twitter – assuming Dave was short for David, rather than Devanand. It’s circumstantial, but the fact Morrison doesn’t know his actual name strongly contradicts a narrative in which the PM and Sharma are conspiratorially entwined.

This struck me as extremely immoral, especially because of the flippant reference to the vaccine causing blood clots, a serious issue that has fostered a lot of anxiety. For a media professional to, without any evidence, lay these complications, including several deaths, at the feet of the PM, and to imply they are the result of a corrupted decision making process – that the vaccine roll out is being guided primarily by the interests of health company shareholders and/or political insiders – is wrong in and of itself. The fact that it also feeds vaccine conspiracy theories makes it even worse.

If clicking “view entire research process” doesn’t work, Right Click and chose “open in new tab”

The third statement I found to be less than half true (I scored it 0.3) is that Morrison gave the vaccine roll out contract to a “personal mate”. It was not immediately obvious whether this should be a checkable claim, since it was said in a comical voice, meant to be the PM’s. But given the context of other similar accusations, and the decision to flash a source article on screen, it seems to me that a reasonable person would think this was meant as a serious claim. But once again FJ is misrepresenting the content of source material which they flash on screen. The source article uses the words “Mates Not States” but does not claim Morrison gave the contract to a personal mate. Rather it points out donations by these companies to the Liberal Party (as well as smaller donations to the Labor Party) and previous government contracts awarded – implying an unseemingly cosy institutional relationship between these big businesses and the liberal party, rather than personal corruption by Scott Morrison.

The fourth claim to receive a sub 0.5 ranking (0.3) is that the Morrison government gave “the contract to companies who don’t even do this thing”. In this case, FJ is directly and accurately quoting the source they show on screen. But this source, an article by Andrew P Street in Independent Australia, contradicts itself a few paragraphs down, describing a contract given to one of these companies earlier in the pandemic (to raise concerns over the size of said contract). On their own website, one of the companies also discusses testing and other tasks they have undertaken during the pandemic. Given that they are healthcare companies, it is not, as FJ opines, like having the Kraft food company build a road.

The fifth claim to receive a 0.5 score or lower (it scored 0.5), and the last I will detail here is that “Former Labor Minister Greg Combet designed JobKeeper for them [the coalition]”. FJ goes significantly beyond what the source documents they reference describe, creating the impression Combet was the primary architect of the JobKeeper program. Rosslyn Beeby, whose article FJ cites, describes his role as ”to report on the workplace impacts of Covid-19”. This other article, by The New Daily – which Jordies cites elsewhere and so presumably considers reliable – describes the role as providing “strategic and policy advice to the minister”. I would add that it is a sad indictment of our political culture that reaching across the aisle for expertise is seen and presented as a sign of failure.

Obviously there are also seven claims that I have rated as entirely true, three which I have rated as mostly true. I have not detailed those here, just as you wouldn’t, in a news article, focus on the majority of customers who do not get salmonella from a particular restaurant, or the two of three passengers an Uber driver is taking to the correct locations before taking every third to a random incorrect location. You can see a table containing all the claims, their sources, and my findings, here.

I am aware that this comes at a bad time for FJ, since they are already involved in one libel suit with the deputy premier of NSW. I have no comment on that case whatsoever. His producer is also facing criminal stalking charges over approaching the same person. Similarly, I make no comment about this case, except that it is extraordinary that any politician would attempt to criminalise scrutiny, however close, from a member of the press or public.

In the meantime, the Friendlyjordies channel is still producing content, and this content should still be subject to scrutiny of its own. I also speculate that those within the progressive movement who sacrifice accuracy for short-term wins (mainly on social media) contribute to a climate of confusion and disinformation which ultimately undermines progressive goals.

Protected:

The Monetary Political Compass

Two areas where there’s increasing discussion in terms of economics are the issues of monetary theory and basic income. By putting attitudes towards UBI on one axis, and attitudes towards money creation on another we can create a kind of monetary “compass”, to help us navigate this intellectual terrain.

I drew this up to visualise where various thinkers/ideas fall in relation to the three economic ideas that are most interesting to me. A simplified version of it ended up in this essay of mine Remittances From Nowhere in which I argue for a Consumer Monetary Theory style basic income at the global level.

But I still had this more detailed version in my notes so I decided to give it a bit of a polish and share it in case it’s useful to anyone else. There’s also no methodology here beyond my own guestimation, and the choices of who to include are arbitrary and reflect my own interests rather than any kind of representative sample. That is why the bottom right corner, where unconventional thinking about both the desirability of employment and the nature of money collide, is over-represented — as that is where I see the potential for a kind of cambrian explosion in economic thinking to originate. There’s nothing to stop others placing thinkers that interest them within this matrix.

Let’s have a look at the people and positions in a little more detail:

Brittany Hunter (1). Writing for the Foundation for Economic Education, Hunter lays out the conventional thinking on the topic well. She is hostile to the idea of a basic income in the US context on at least two fronts. Firstly it will demotivate workers, secondly it’s two expensive, which would ultimately place an unfair burden on tax-payers, whom, she assumes, are the ultimate source of all public spending. Money in this paradigm is assumed to be essentially a neutral medium of exchange. Real economists, so they say, don’t actually think about money, which is merely a veil over barter, out of which it emerged.

Public Policy Discourse (2). Mostly figures in the public sphere agree with Hunter. In understanding how borrowing and spending works, they tend to model governments on households or individuals. There is some serious thawing of this consensus underway at the edges, but in general it still prevails, even during the pandemic. The need to balance the budget is presented as a technical neccessity, not a policy choice. The media presents, and the average layperson accepts, generally, this rule as “common sense”. By default, if a policy is proposed, “how will you pay for it” is among the first questions. Writing for the Poynter Institute, Al Tompkins urges his colleagues in the media to demand answers from politicians about how and when they will pay off all the debt required to pay for the stimulus. He says government borrowing:

It is not unlike you borrowing money when you want to buy a house or a car. Borrowing is not always a terrible idea, unless you do not have the income to pay the loan back. Federal spending works the same way.

Paul Krugman (3). On the leftward fringe of the mainstream spectrum are figures who balance the pressure to conform to this mainstream thinking with the need to maintain some contact with economic reality. One such figure is Krugman, an economist best known through his analysis and opinion work published in the new york times who will say things like “no, we don’t have to worry about paying off the debt; we never will, and that’s OK,” and link to this blog post by Morgan Housel, which explains that a government escapes debt by out-growing it, so that while absolute debt grows, GDP grows faster. This means that the debt to GDP ratio stays manageable, as do the obligations regarding interest and payments.

What neither of them suggests is that government spending could be (indeed is already) funded by simply creating money. That they implicitly leave to banks, including the quasi-private, nominally “independent” central reserve.

Those banks, he notes, are lending at phenomenally low rates. This makes it even easier for the government to borrow money, invest, and reap the rewards as economic growth in time to pay off the creditors, protecting future tax paying generations from crushing obligations.

There’s no doubt that he or she understands that money is a just social construct. They have been convinced though, that the inherent rules of money include a taboo on just printing more of it ,“on demand” as it were, or the fiction would collapse, and money would suffer a catastrophic loss of value. He might be naked, but he’s still the emperor.

Public Policy Practice (4)

The reality is that governments rarely balance budgets. Deficit years outnumber and out punch the surplus years, and interest piles on top of that to create an ever growing mound of debt

The 90 years of consistent deficit spending shown in the graph above (sourced from whitehouse.gov) has left America a more developed, better off, nation than it had been at the start.

Politicians always promise one thing, then end up doing another. But in this case what they promise is wrong and what they end up doing is right. The system would collapse if they did otherwise and always finds a way to force the decision makers hands’ into deficit spending as a perpetually temporary measure. Like now.

There’s always the possibility of too much of a good thing — when government largesse causes economy wide spending to outpace productive capacity and cause inflation — but below this threshold the general rule is that the more the government spends, the richer the nation becomes.

Stephanie Kelton (5)

Kelton’s approach is to advocate that governments should own up to reality and come out of the closet as deficit-lovers. Her reasoning for why this is ok is far more straightforward than, say, Krugman’s: A government with it’s own currency can’t go broke. It could just print money. There’s no reason it would ever default on a debt denominated in its own currency. Governments don’t tax and spend. They spend, then tax.

In conventional thinking, taxes fill a bucket, the “government coffers”, and spending is the hole in that bucket, through which money escapes. According to “Modern Monetary Theory”, which Kelton advocates, it’s not so much a bucket, but a flower-pot, waiting to be watered, and this doesn’t represent the government’s “coffers” but instead the economy. Government spending is the flow of money into the pot, and taxes are the drainage holes, the outflow which need only match inflow once the soil is saturated. Their purpose is to stop the water overflowing, which would mean more money chasing after goods than the economy could handle, and therefore inflation. Taxes are demanded by a government in a specific currency to help ensure it’s value. But the quantity received needn’t match spending. It shouldn’t.

The position isn’t so much, as it is sometimes described, that deficits don’t matter. It goes further. Deficits are mostly good. Surpluses are mostly bad. It’s the accumulate public debt that doesn’t matter. It’s just a historical record of what happened.

The real limit on spending, as described above, is production. The penalty for overshooting this limit is inflation, not bankruptcy.

But even with all that extra capacity that gives the government to spend, MMT advocates like Kelton still don’t think a UBI is a good idea, except perhaps as an emergency measure during the pandemic. This is partially because they believe a UBI would increase spending without increasing production, whereas the policy she does advocate, a job guarantee, would increase them in tandem, since the government created jobs would either be productive themselves (producing goods and services) or increase productive capacity (building infrastructure). I and others question this straightforward relationship between employment and production, noting that make-work could use up more of the economy’s resources than just giving people money, requiring equipment and transport and clothing and other items.

But Kelton has also defended working in and of itself as better than not working — not in the moral sense that a person should contribute, but in the sense that it is better for the person working to be working than it would be for them to be passively receiving income, which she contends would cause them to be depressed and isolated (as if work is universally enjoyable and fulfilling, and leisure is universally not), and as if a basic income and employment are mutually exclusive — whereas the whole idea is that (unlike work and unemployment payments) they are not.

She and other MMT advocates decry the evil of involuntary unemployment, but are unconcerned with involuntary employment — people who would rather not work who are forced to by the threat of poverty.

Andrew Yang (6) Yang, who ran in the US Democratic primary on the idea of a $1000 a month UBI funded primarily with a value added tax thinks robots are coming to take our jobs. Since his primary run he has joined with other politicians to call for emergency payments of $2000 a month to all Americans during the pandemic.

Karl Widerquist (7) Widerquist is an American philosopher who critiques Hobbesean and social contract theories of private property, and supports the UBI as a way of addressing the injustice inherent in the inequalities and unfreedoms our society imposes on people. He has produced costings for various models, emphasising that the “net” cost -after a proportion or all, of the UBI is taxed back from wealthier recipients through a progressive income tax — is lower than the gross cost, and relatively affordable.

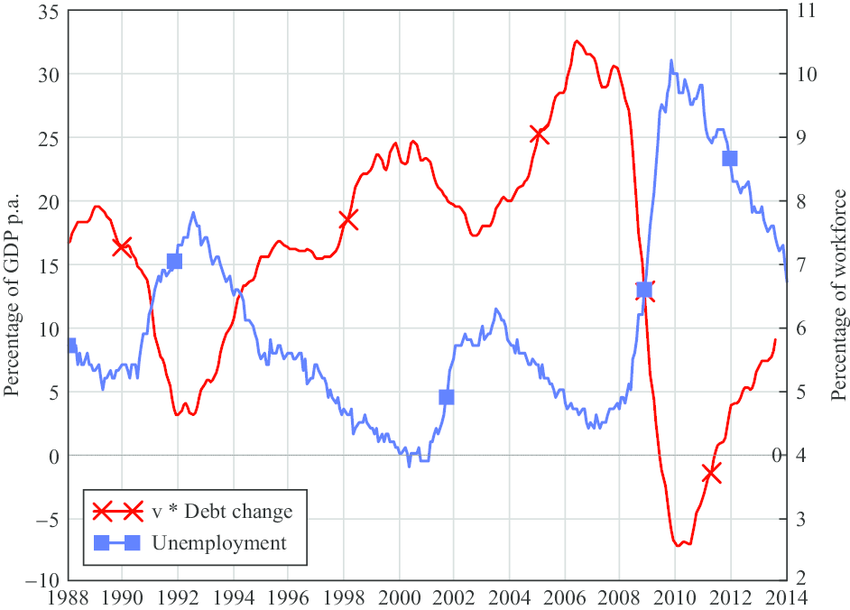

Steve Keen (8) Keen is a leading post-keynesian thinker, unique in his focus on the role of private debt in the economy (and more recently on energy, but that’s beyond the scope of this article). This focus on the macroeconomic effect of money creation by banks led him to predict the 2008 crash. His interpretation is also backed by his ability to identify impressive correlations between debt and other economic indicators, as shown in the graph below showing change in debt and unemployment:

He’s also created his own modelling software called Minsky (after the economist Hyman Minsky, who he considers an intellectual predecessor. On the basis of this body of theory and modelling, he backs both debt jubilees and a basic income.

Geoff Crocker (9) Crocker combines soft currency theory with a close look at technologically driven labour market trends (of the kind Job Guarantee advocates ignore, or hope to somehow overpower). One point he makes repeatedly is that consumer spending has already overtaken aggregate wages making unearned income a mathematical necessity. Both in the sense that it is, factually, a part of the economy already, and in the policy sense, that it needs to be provided to people fairly to prevent inequality and poverty. He suggests the creation of “debt free” sovereign money by central banks, distributed to people as a basic income. Whereas Steve Keen often points to the issue of private debt as a problem, Crocker argues this is only a proximate cause and the root cause is productivity growth outpacing wage growth, neccessitating non-wage income to fund consumption. Easy credit has been filling in the gap, but basic income should instead.

Alex Howlett (10) Howlett’s position is close to that of Crocker’s but he doesn’t see the need for explicitly debt free “sovereign” money creation, arguing that deficit spending and central bank behavior as currently structured is sufficient to achieve the same ends. He is also less concerned about inequality than Crocker, arguing that the immense wealth of billionaires, for example, being mostly tied up in stocks and other assets, and doesn’t compete with the spending of ordinary people for consumable resources.

Howlett is, even among UBI advocates, far more explicitly skeptical about the value of employment as a goal. Keen or Crocker might (seem to) be saying that full employment would be nice, it just isn’t possible or isn’t sufficient to overcome structural issues around money creation. Howlett explicitly argues against employment as a goal or explicitly desireable outcome. It is instead an input-like any other resource, which should be used as efficiently as possible to achieve production.

The labour market is a way to get people to do things they wouldn’t do for free, and shouldn’t be the way we get money to people for consumption — a UBI should be. He also describes a change in housing markets as a bonus effect of decoupling income from work, since people could move away from the major job markets (and stimulate depressed regional ones).

Howlett emphasises that in a functional economy, money would flow to consumers to producers, but that process is blocked because we expect money to flow to people primarily as a result (rather than a cause) of their productive labour. He calls this Consumer Monetary Theory, to distinguish this approach from MMT. and often uses the metaphor of the economy as a “giant vending machine”.

Oxfam (11)Oxfam advocates for a kind of Global MMT — suggesting that the IMF issue Special Drawing Rights, to developed nations. Theres are a unique interest bearing financial asset, which only governments can hold, and which are exchangeable for cash and can be used to pay back IMF loans.

This would give poor countries the liquidity they need to protect their populations from poverty. This was advocated lastyear as a response to the pandemic and its economic fallout. It might sound wild, but it’s happened before (in 2009) and the IMF is, or atleast was, apparently considering it.

World Basic Income (12)The NGO which advocates for a World Basic Income funded by “rents” on the global commons. These include a Carbon Dividend, Aviation Fees, Ocean Revenues and others. But they also say money creation could be used in extraordinary circumstances, such as now during the pandemic.

Me (13) I argue for a combination of the Oxfam and WBI positions — which ends up being very similar to a global version of Crocker’s proposal. I think the IMF should create accounts for every human being over a certain age and deposit into it a new digital currency which it could then guarantee the value of by allowing governments to purchase SDRs with it in auctions, or by charging a tax on national governments denominated in it. By giving it value to nation states, the IMF would encourage those nation states to exchange their established currencies for it. In the essay where I first proposed the idea, which frames the proposal as an emergency response to the coronavirus contraction, I suggest we could simply make this tax payable by each government in proportion to the total amount received by their citizens in WBI payments — so the government would be compelled to buy some proportion (say 10%) of the newly issued currency from its citizens, or accept it as tax payment, thereby validating it. In an as yet unpublished manifesto with political as well as economic content, I and other authors place this idea in the context of the longer term project of building a broader global state and suggest the tax could instead be charged in proportion to national military budgets, thereby helping drive a general disarmament.

In either case the tax would create demand for and validate the currency the WBI was issued in, and give it purchasing power which would dramatically reduce poverty, and reshape global labour markets, lowering cross-border wage competition without creating the contractionary pressures of tariffs and trade wars might.

I see this as uniquely addressing the contractionary pressures of decades of neo-liberal austerity and the dislocating effects of globalisation, which have combined to disempower ordinary people in developed and developing nations.

Our Bullshit Economy is Doomed.

We are completely, bowleggedly, phillips-head screwed.

Heard about the guy who fell off a skyscraper? On his way down past each floor, he kept saying to reassure himself: So far so good… so far so good… ― La Haine

The headline popped onto my screen unasked for, in a notification from google news: Stock Market Hits New Highs on Stimulus Hopes.

Morons, I thought. They still don’t get it. They still think that the stock market (or bitcoin, or housing) is high despite the weakness of the real economy. If it’s doing so well now despite the contraction, imagine how good it will do when mainstreat comes roaring back to life?

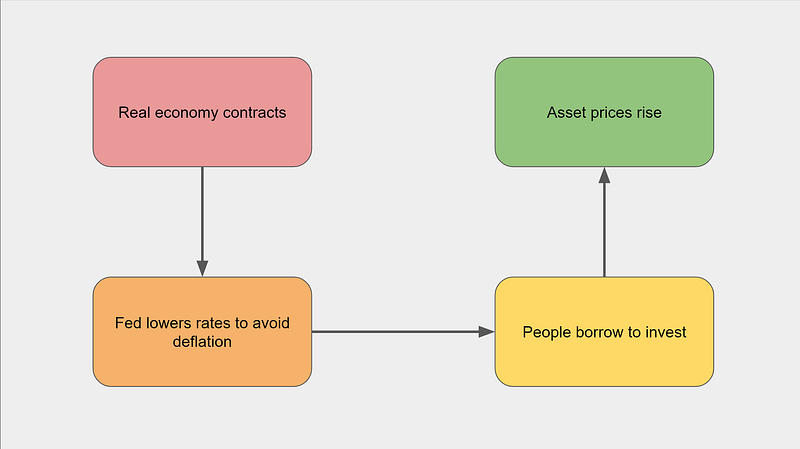

But wall street is high because of the weakness of the real economy. If the virus recedes, and if the real economy starts to actually thrive (two big ifs) then the fed — in line with inflation targeting — will have to increase interest rates. New loans will slow, and those who have borrowed to invest need to start increasing their repayments. Suddenly the bear will roar and the cheap-debt fuelled orgy of greed will come to a screeching terrified halt.

Of course some of the companies will benefit from the stimulus induced increase in main-street spending. That will allow them to pay higher dividends, theoretically allowing their shareholders to cover these repayments. But everything would have to line up just right. The minimum wage/tip workers who get re-employed by restaurants, would all have to go out and buy Teslas, or at least the restaurant owners would, assuming Tesla is even able to meet that increased demand, to justify that stock’s rocketing price. Maybe. And maybe Amazon sales will increase, with the shift to online retail proving permanent. But what about Signal Advance? The health care company whose stock price increased by over six thousand percentage points after Elon Musk tweeted about an encrypted chat app of the same name? What about bitcoin? Will it suddenly start paying dividends?

The core attraction of these investments has never been returns, but equity growth. And the thing about equity is you can’t actually spend it, or use it to repay the bank. You have to sell to do that. And that’s fine, so long as there are fresh buyers, but if QE and low interest rates disappear, those buyers won’t be there. And just like that *poof*, all those gains are gone.

Or worse, they aren’t, because interest rates stay low, because the real economy continues to operate under capacity, and the “K shaped recovery” continues, meaning the rich get richer while the middle class stagnates and the underclass precariat grows. Then the correction will end up being of an entirely different, political, rather than economic nature, which could be far more terrifying indeed.

The way things are set up now, it’s wall-street vs main street, and it has been for a while. The combination of austerity thinking and inflation targeting by central banks, introduced in the 80s and 90s respectively, dislocated the already tenuous relationship between the stock market and the real economy.

It works like this: The government pulls back on spending and suppresses wage growth, despite growing productivity, so the economy veers towards a deflationary spiral. In steps the central bank, lowering rates and buying excess debt out of the economy and voila, inflation stays in positive territory. Stocks rise on the back of leveraged investments, cash-poor middle class households convince themselves that they are actually brick-and-mortar millionaires. They let the credit card rip (or borrow against their equity to spend), and for a time, it is good. But larger and larger sections of the population — those who never had a chance to acquire assets- are left further and further behind.

If the government steps in on the fiscal side of things, to boost the spending power of those left behind (and help the middle class with those credit card repayments) then we’ll see real inflationary pressure, and rates -according to the technocratic religion of Independent Central Banks — will go back up, spelling doom for asset markets.

How did we get to this dangerous impasse?

This is to do with the fundamental role of banking and money in the economy. Something mainstream economists, politicians, media and investors studiously ignore.

When interest rates go up, money flows faster out of the economy back into the financial sector, new money needs to flow the other way, in the form of new loans. Our bullshit economy is dependent on ever increasing levels of debt, on an ever greater fool willing to take on that debt.

When the music stops, someone is going to be left holding the bag. The longer that takes, the bigger the bag will be. The more “ma-and-pa” investors get in on the action through gamestonks or smartphone based crypto trading apps, or over-priced investment properties, the bigger their share of the stinky excrement will be.

So if a Biden administration does proceed with the promises made to the Bernie faction of the democratic party, they will be undermining not just their wall street backers but the upper end of the suburban middle class, a core voting block they just won over from the Republicans.

Either way, unless our leaders embrace radical new thinking, the pain is coming.

It might be possible to square the circle and avoid that pain, balancing a slow deflation of asset prices with an increase in incomes and spending, but that would require a government that actually understood the problem. That would, in turn, require a lot of high status people to admit they were wrong and adopt new ideas. And it seems unlikely that will happen until after things go from fraught to catastrophic. Until then it will be a case of “so far so good… so far so good…”

How a Basic Income could Lower Housing Costs.

The inflationary effects of a basic income would allow central banks to raise interest rates, slowing the flow of money from the financial sector into asset bubbles like stocks and, crucially, housing.

One of the most common objections raised to a basic income is that house prices and rents will simply be raised and erase all the income gains, leaving people back where they started. Even if all other factors were held static it seems likely that competition between landlords and home sellers — and with those selling other asset classes — would act as something of a brake on price increases, preventing them from absorbing all of the increase in income.

But other factors won’t be held static. For a start there would be a decoupling of the labour and housing markets which would increase vendor-side competition in the housing market, since there would be a greater number of people who could quit their current job and move where housing is cheaper. This would compliment and overlap with the existing trend towards remote work. The increased spending power and arrival of new customers in country towns would then create more employment opportunities, making them even more attractive relative to the city. It would of course put upward pressure on regional house prices, but across the whole economy the spread of demand would lessen pressure on city markets.

In Australia we’ve recently got a sense of the short term limits of this effect, as the pandemic increased city-to-country transitions, especially along the east coast, causing house prices in regional areas to rise, often pricing out locals. But in the longer term new housing stock could easily be added in these areas — at lower cost than in the cities.

But there are other factors lurking behind those rural price hikes, the same factors which prevented a collapse of house prices in the city, despite the biggest economic contraction on record.

Part of it is the Jobkeeper wage subsidy and increased Jobseeker unemployment payments, and the government allowing people to access up to $20k of their retirement funds, and directly incentivising home building and improvement (my family and I were recently evicted so my landlord could renovate, which the government was incentivising to the tune of $25k).

But the bigger part is simply cheap credit. House prices have remained high for the same reason the stock market has remained high: Because interest rates are effectively below zero. In the US is what’s been called a “fed driven economy”. Cheap money for those who already have assets and/or a good credit rating has sustained and even expanded what was already a huge asset bubble. You can borrow money, buy tech stocks, bitcoin, gold, or some other relatively safe asset -like real estate- and watch the value rise at a rate which far outstrips the interest on your debt.

This wasn’t the goal of central banks but a side effect of them crashing rates, in a desperate attempt to stimulate business activity, and fend off a great-depression-like economic catastrophe. It hasn’t totally failed, or been a huge success. It’s hard to tease out the causality, but my suspicion is that fiscal policy is what has kept the deflationary spiral at bay. Monetary policy has helped by supporting that spending with bond purchases. Low interest rates, on the other hand, have mostly fuelled the credit driven asset bubble — which can never be a good thing in the long term. Sure some businesses might stay afloat that wouldn’t have otherwise, but putting money in consumers hands would have had a much more direct and powerful effect, without increasing the instability in the financial sector. Similarly there are those who have avoided selling their house because interest payments were low — but increasing their incomes instead of lessening these payments would have solved that problem too, without inviting leveraged speculative investment.

A basic income would likely be, overall, (though not exclusively) inflationary. This would allow central banks to raise interest rates from their current record lows. That would increase the cost of borrowing, including mortgages, which would discourage asset speculation, including housing. The higher we make the basic income the more spending power it puts into people’s hands and the less we need to stimulate the economy (and asset pricess) with cheap credit.

The hardest question, as usual, is what do we actually want to do? It seems unfair to punish those in the middle class who have invested heavily in housing as an asset, and who were encouraged to do so by policy makers. But the current situation punishes all those below this stratum, those looking to buy their first home, struggling renters, and finally the housing insecure and homeless.

Perhaps the goal of a catch-up period, where house prices hold steady (in adjusted dollars) while the economy and incomes grow around them is the consensus point we can settle on. We could even aim for modest growth in real terms, so long as growth in incomes and the economy as a whole outpaced this, meaning the percentage of income spent on housing would shrink.

To achieve this balancing act, however, we will need a clear picture of what got us to this point.

Even before the pandemic there had been a long period where overall conditions were predominantly deflationary, with inflation in Australia and many other major economies staying below the target range despite historically low interest rates. Attempts to raise these rates threatened to stall economic growth, so in 2008, then again from 2011 onwards they hit record low after record low.

This year rates dropped to just 0.1 of a percentage point. But even this combined with record government spending is only just enough to keep inflation in positive territory. But that’s just the pandemic right, suppressing spending? Actually not so much. Consumer spending is in fact at record highs in Australia! Especially spending on goods (and housing), rather than services. But with our mostly low case numbers, even restaurants are doing well.

There are deeper, long term trends at play that the pandemic has merely accelerated. Consider the following graphs from the Reserve Bank’s website

To understand these trends we have to properly understand the role of the banking sector in the economy, something mainstream economists are loath to do. Economists point out that on some level, money doesn’t matter. The point is the stuff it buys. This is of course, on some level, correct. The point of the economy is to make and distribute things, and provide services.

Obviously, however the people at the end of these supply chains need money with which to purchase these goods. So how does the current system -where there is no basic income- get them this money? Primarily through the labour market, which the banking sector and ultimately the central bank stimulates — or tries to — with lending.

But as productivity rises, less and less labour is needed to create the same — or even greater — outputs. This effect has been concentrated so far in the production of goods (rather than the provision of services), where globalisation and automation have combined to drastically reduce the need for labour, and increase productive capacity. There are now fears that automation will come for the service sector, too — but why should we be afraid? Why is having fewer people (and more machines) serving coffee and guiding tourists really such a terrible thing?

We are afraid because without jobs people become destitute. People go needlessly without, while productive capacity stands idle — the obscenity of housing insecurity and homelessness while many houses go unoccupied, for example. But basic income (which recent polling shows 58% of Australian’s already support, and only 18% oppose.) can fix this. Poverty can be abolished.

I don’t propose this strategy as a panacea. If the government got everything else wrong — in terms of public housing policy, the balance of infrastructure and immigration rates, and and so on — house prices and interest rates could rise simultaneously.

The capacity of the political class to fuck things up is inexhaustible. But sometimes, when enough pressure is applied, they can get things right, too. So it’s worth thinking about what that might look like.

We could increase minimum wages, and support unions who fight for higher pay in the private sector. We could increase government spending including both wages and employment numbers in the public sector. And we should do both those things.

But the simplest and best way to get money to people is to give people money.

So what about raising the unemployment payments? Yes. Good. That too.

Often it is assumed that these would be eliminated with the introduction of a basic income. But this need not be the case, these targeted and conditional payments could remain to lessen the income penalty for the involuntarily unemployed, and to incentivise and support (re)-entry to the labour market, so long and to the extent that we as a society think that’s desirable. Similarly student, parenting and disability payments could continue, stacking on top of the universal amount to support and incentivise socially valuable behaviour, and compensate for unfair disadvantage.

This would allow us to ramp the basic income in over time, rather than all at once. Everything else stays the same, and everyone with a Tax File Number and a bank account associated with that number gets a small but non-negligible amount, say $50 a week. Then when the sky doesn’t fall, we ramp it up towards (and maybe even beyond) a livable income while watching the effects on other indicators, like inflation, interest rates, inequality and housing prices, the labour market, adjusting the payment and/or other policy settings as we go.

This gradualist approach would allow us to balance the risks of doing too much against the risk of not doing enough — which is perhaps right now the greater danger.

Nobody is Born Alone

The phrase is a cliche: “We’re born alone, and we die alone”.

Some minority of people may, by mishap, despite our best efforts as a society, die alone. But mostly they are nursed in their deathbeds.

But actually, literally, absolutely no one is ever born alone. Even in the extreme case, the most isolated birth possible, the baby is still not born alone. The mother is, by definition, always there. My sister recently gave birth to twins. So there were three people involved intimately in the event, at the level of direct participation, then a circle around them of professional carers, mixed with family members, who would have willingly ripped their own hearts out to prevent harm to the newborns or their mother, and around them a broader community all emotionally invested in the well being of the family unit. This is all fairly typical.

If we apply the principle of charity and attempt to find the kernel of truth in this statement, we might say that what they are referring to is the uniqueness of our experience. Your mother might be there physically with you, but she remains a separate consciousness, a whole other person, trapped in her own body, from which you have now been expelled, exiled into your own bag of skin. The bitterness in the phrase, then, speaks of an unsatiated desire for an impossible union, a dissolution of multiple selves into one. But would not that simply create a super consciousness, now occupying two bodies, but as alone as ever?

It is the impossible desire to transcend the self and its finitude, without losing it’s unique identity — to assimilate and absorb the ones we love, which would obliterate them.

This phrase is an expression not of reality, but of an ideology of obsessive individualism, in which vulnerability, the need for kindness and love, are taboo, in which we remain infantilised, unable to navigate the boundaries between ourselves and the world, between ourselves and other people — to see them as a seams, rather than as barriers.

The error is similar to that made by those who declare that we cannot have free will, since decisions are merely the results of charge levels and random outcomes in subatomic particles in atoms in the molecules in the cells in our organs in our bodies. But if we believe we are our bodies, then we are those atoms, those charge levels, those random outcomes, and the decisions are ours. Implicit in the position that physicality negates free will is the yearning for some kind of self that is both separate from yet identical to the embodied (and deeply connected) self we experience being each day.

You are not alone. You have choices. Don’t let the booming voice of ideology tell you otherwise.

German Reunification and De-escalating Labour Market Conflict through a Basic Income

So I have been watching the Netflix doco “A Perfect Crime” which focusses on the assisination of Detlev Rohwedder, who was the head of Treuhand, the responsible for reforming the East German economy after reunification.

The context of the crime is the conflict between the needs of labour and the needs of capital. East German industry had been set up to make sure everyone had a job, and that those jobs paid well. But the firms were not efficient or competetive in the global market. Making them competetive meant massive economic pain for ordinary East Germans — wage cuts and, especially, job losses.

Here we have a microcosm of the essential class conflict that had driven much of politics in the developed world since the industrial revolution. Capital wants to cut labour cost, workers want to get paid more. Globalisation and cross border wage competition is one face of this problem, but not the only one. Let’s say automation comes along as some predict, and employing people *anywhere* becomes inefficient. Do we deliberately keep doing things the innefficient way as an excuse to give people money? How can doing more work than is needed really be in the interest of workers as a whole?

The problem is we are asking the labour market to do two things at once: efficiently produce goods and services, and provide incomes to support household consumption and prevent poverty. If the basic income is how we support consumption, and the labour market is just for getting things done, we can have it both ways.

This is what some on the left don’t like about a basic income, it deconflicts the labour market. They are so busy worrying about escalating the conflict and winning the fight, they have forgotten what it is we’re meant to be fighting for: decent lives for ordinary people.

They don’t want a way around the fight, they want some kind of (impossible) final and decisive victory, in which the interests of capital are forever vanquished — but that would mean a loss of the drive for efficiency, economies of scale, and so on — which means, as a whole, more work and less stuff for everyone.

If we solve distribution through a basic income, we can allow capitalists to be as ruthlessly efficient as they like, and all those efficiency gains will allow us to pay a higher basic income before we hit the inflationary limit of too much spending and not enough to spend it on, so productivity growth means greater prosperity for all.

But there will still be a labour market where, and this is what I think the left-opponents of a basic income get wrongest, labour has a stronger hand!

They seem to think that because they aren’t fighting for survival, or because they have lost some moral argument about the need for higher wages, workers will accept shitty pay. That might be true in some areas where people really want to work (media, politics, etc). But I think overall the opposite will be true.

People will need wages less, so they will be in a stronger bargaining position to demand more. Many people will leave the workforce entirely, others will work fewer hours, jobs, or years. The overall supply of labour will be constricted, while the demand for goods and services rises. This will give workers — who collectively have guaranteed strike pay, and as individuals always have the option of walking away — immense bargaining power and the wage share of income relative to profit will increase, not decrease.

Explaining Bullshit Jobs with Monetary Theory

It’s as if someone were out there making up pointless jobs just for the sake of keeping us all working. And here, precisely, lies the mystery. In capitalism, this is precisely what is not supposed to happen. — David Graeber

The recently deceased anthropologist David Greaber’s seminal essay, followed soon after by the book, “Bullshit Jobs”, was undoubtedly one of the most impactful intellectual efforts of recent times, being translated into several languages, resonating with people across the globe and becoming a touchstone of political and economic discourse.

Graeber has no trouble identifying the what of the problem — work so frivolous that even the person doing it agrees that it serves no real purpose. He also proposes a somewhat convincing reason why:

The answer clearly isn’t economic: it’s moral and political. The ruling class has figured out that a happy and productive population with free time on their hands is a mortal danger (think of what started to happen when this even began to be approximated in the ‘60s).

This might be part of the story, but whatever the “moral and political” imperatives of employers as a class, there is a strong individual incentive for them to minimise their labour costs. What is the mechanism, the how, by which their supposed collective interest wins out?

Employment is, by definition, work performed for money. Therefore labour (like other resources) moves in the opposite direction to currency. I made a rhyme so it’s easy to remember: From whence money flows, there labour goes.

There are exceptions to this, when money flows up, away from workers -taxes and loan repayments for example- but those are both times when money is flowing out of the real economy.

So from where does the money flow in? Well, actually, the same places: banks and the government.

Banks create money in the form of an account balance when they authorise loans. These accounts are, economic textbooks falsely argue, backed by a reserve of central bank money, created in the same manner. But in reality banks lend first, then top up their reserves after the fact.

Bank lending favours the wealthy and large companies, since banks are more inclined to lend to people and businesses with existing assets and high incomes. This will be important later on.

But first it’s important to note that governments also create money. The government borrows by selling interest paying treasury bonds to investors and banks. Then, as needed, the central bank buys these bonds from those investors and banks with money it creates with keystrokes. So called “modern monetary theory” isn’t just an idea for what should happen, but also a description of what already happens.

There’s more to it, but for the purposes of this post, what matters is that proportion of money entering the economy from one of these sources vs the other changes over time.

The post-war boom was the product of sustained and substantial deficit spending. This government largesse put money in the hands of ordinary people who spent it on products and services -made, sold and delivered by other ordinary people — causing widespread prosperity, like how a whole ecosystem becomes more vibrant after a big rain.

Since the 70’s, though, the fashion in economics generally has been to laud the private sector as “wealth creators” and demonise the public sector and government spending, often by way of the false premise that it must be “paid for” in taxes.

That means the right hand side of the graph above has come to dominate over the left hand side, and pull labour away from things which have direct value to consumers, and towards things which have value to businesses.

So you have experts consulting on tax law to design companies who are contracted by advertising companies who are engaged by companies that make software for lead generation for companies who run corporate team building retreats for law firms who provide patent expertise to venture capitalist firms who invest in blockchain technology companies who provide services to banks who, maybe, lend money to companies that, finally, actually make products for customers to use in the real world. Or not. The real world, after all, is not where the money comes from.

This helps explain how, fuelled by cheap money provided by the Federal Reserve the US stock market has continued to rise even as the real economy has collapsed.

Of course this kind of networked specialisation can be used — in the right macroeconomic conditions — to create an efficiently modular system. Each company doesn’t need it’s own tax experts or designers or whatever but can bring in specialists as needed. These specialists will — by providing services to many different companies — have certain economies of scale. But these aren’t the right macroeconomic conditions.

It’s also true that some of the jobs driven by consumer spending are not worthwhile, or at least not very worthwhile. When consumers don’t have much money, and workers are prepared to work for low wages, people will spend small amounts on low value products at businesses that pay shit wages. If they had more money, they would buy more expensive products and businesses could pay better wages, invest in better equipment and generally be more valuable as enterprises.

We’ve had a hint at what might happen if these low-worth jobs were eliminated during the pandemic. Australia saw GDP contract by 7% over the 2019–2020 financial year, but saw GDP per hour worked rise by 4.1% over the same period. Most of that is accounted for by a particularly dramatic 3.1% increase in a single quarter, between just March and June of this year, as the lockdown kicked in, as roles for receptionists and waitstaff were terminated — but high value jobs continued (leaving aside the question of whether the market is currently valuing things correctly, which it isn’t).

More fundamentally, it’s not even true that all jobs driven by consumer spending are actually driven by consumer spending. A great deal of what we count as consumer spending (transport for commuting, clothes for the office, sandwiches and coffee purchased at the cafe at the bottom of the office building) is actually to do with working which is, in theory at least, about production, not consumption. Having a job is expensive. The most privileged and in demand workers, like a-list engineers working at the big name tech companies, it is worth noting, are not expected to cover these costs. They get free food at work and buses to bring them to the ‘campus’. But the rest of us are not so lucky.

All this work-related expenditure funds what Medium’s editor at large Steve Levine calls the “The Hidden Trillion-Dollar Office Economy”, which, he laments, remote work is “killing”.

He rightly points out that “a massive part of our economy hinges on white-collar workers returning to the office” but fails to consider what that tells us about the fundamentally wasteful nature of our economy. Instead he worries about the fate of food delivery services, dry cleaners, printing and office supply stores, Starbucks, the business wear chain Brooks Brothers, and even real estate. Discussing this final example he asks:

It will save these companies leasing costs and their employees their commutes, but at what cost to the rest of the economy?

But, unless we think work and economic activity are inherently good things, ends in themselves rather than a means to providing people with products and services, then for the economy overall it’s not a cost. It’s a saving.

When making rockets engineers and scientists work hard to minimise and overcome what they call the “Beer Can Problem”. You start with a payload you want to deliver to space — some astronauts who need to get to the space station or whatever. Then you need the fuel to lift them into orbit. Then you need the fuel to lift that fuel. Then you need the fuel to lift the fuel to lift the fuel. And so on. Pretty soon the rocket is like a tall explosive beer can, only heavy when it’s full.

We can imagine the economy facing a similar problem. We need a certain amount of labour to make, transport and provide the stuff and services we actually need, or even want: food, housing, education, healthcare, plumbing, electricity, consumer economics — directly useful stuff. That’s the payload.

Then there’s the labour of management, admin, banking, lawyering and even some amount of sales and marketing, and so on required to support these industries. That’s the fuel that lifts the payload. Then the people performing this labour need office space and transport and electricity and so on to function, which requires more labour. Then that labour needs administrative support and so on, until you have massive city centre office towers filled with paper pushers far removed from the direct production of useful stuff, and 24 lane freeways, which are not need to deliver goods to consumers or let people move around for leisure and consumption, but to handle the commuter rush-hour and get people all to work on time. Then we need concrete suppliers, who need factories, for which we need architects who need accountants who need…

This could be viewed as our economy-wide version of the Beer Can Problem. It is to some extent unavoidable. But it could — especially with increasingly advanced information technology — be minimised.

But we don’t view it as a problem. Instead we view it as a solution; to the problem of not enough work. We don’t seek to mitigate and manage it, we seek to enhance, expand and maximise it. Jobs! Jobs! Jobs!

Problems are solutions. Savings are costs. Work is good. Leisure is bad. Production is not a means to achieve consumption — instead consumption is a means to achieve production.

When the ideological blindfold is removed, we can see the fundamental irrationality of our economic system — a huge headless meatware machine, to which we have all become slaves, which lumbers on mindlessly, dragging us towards a future no one really wants.

This helps us understand two things Graeber got wrong. One of these is placing the blame entirely at the feet of a ruling class he apparently sees as fiendishly conspiratorial and disciplined, rather than just mean and stupid. The second is the attempt to say which kind of jobs are bullshit. Just before his untimely death he wrote:

Whole industries (think telemarketers, corporate law, private equity) whole lines of work (middle management, brand strategists, high-level hospital or school administrators, editors of in-house corporate magazines) exist primarily to convince us there is some reason for their existence.

It’s pretty hard to defend telemarketing. But this kind of demand mining activity (of which Facebook and Google’s zillion dollar ad-placement algorithms are further examples) is really just a symptom of a deeper, structural problem. In a sane economy, where people had money to spend and labour was properly priced, demand would drive supply. Companies would be focussed on making and doing stuff, not coaxing and badgering consumers into making purchases.

Fundamentally it’s not specific kinds of jobs, or companies, or industries, or sectors. The whole economy is infused with bullshit. No job is free of it. Even a large portion of the work performed in the health system is just dealing with the damage our sadistic economy does to people.

The fundamental problem is that money enters the economy in the wrong place. That puts banks and investors and the wealthy upstream — and everyone else, what Graeber would call “the 99%”, downstream, at their service.

The only way for us to get even a drop is to come up with something they want. And what do you sell to the man who has everything? Well, it turns out, maybe some caviar, a superyacht or two and a half-shredded Banksy — but mostly financial instruments, tech stocks, and other vehicles for achieving an ever greater economic power and an ever higher net-worth.

So that is what our economy is fundamentally geared towards.

If the money flowed the opposite direction — if it started with the people and flowed into the economy from there everything would change. Everything.

When it comes to a solution, therefore, I think Graeber is correct, but that he doesn’t quite realise just how correct he is. A basic income, he argues, would allow people to decide what to do with their time. But it’s actually much bigger than that. They would spend it on things they really want, not just the things they need to keep their jobs (like uncomfortable shoes, or housing in overpriced cities) and so our whole economy would start to reorient towards both reducing drudgery and producing what people actually desire, rather than increasing the abstract wealth of a tiny minority.

Unfortunately those who understand the macroeconomic dynamics of money creation described at the start of this essay — proponents of MMT — for the most part fail to appreciate the labour market side of the equation. They have fallen into the same trap and view leisure and freedom from the need to work as a problem, and therefore prefer a job guarantee to a basic income. Only the even more obscure school, really just a cluster of thinkers, who advocate what can be called Consumer Monetary Theory (of which I am a proponent) have effectively joined the dots between money creation and a basic income.

In MMT’s defence, there’s something to the argument that the jobs created by a government program like this (which they say should be federally funded but administered by local councils) might be less bullshitty than those created by the dysfunctional, debt driven private sector.

But to the extent that this is true, those jobs can be created by traditional public sector spending, oriented around goals, which are achieved using the minimum, rather than the maximum amount of labour. Anything else is bullshit job creation, by definition.

Measuring the prosperity of a nation by the amount of work performed in it, or the degree of economic activity is like measuring the value of a book by the number of letters it contains, regardless of whether they say something interesting or are jumbled in meaningless garble.

The best economy is not the biggest (or the smallest), but the most pleasing to the people who inhabit it. The first step towards this is the screamingly, obnoxiously obvious step of just giving people money.

Then we can start to untangle the messy knot we have tied ourselves in, and begin to properly enjoy the efficiency and productivity we have already achieved through technology. Once everything and everyone is pulling in roughly the same direction — towards efficiency and prosperity and away from drudgery and scarcity — further efficiency and productivity gains will be made, and they’ll be made in the areas that really matter. This in turn will allow us to pay a higher basic income, and so on, as the virtuous cycle takes off, carrying us forward towards the Star Trek economy that technological progress clearly makes possible — but which our political economy precludes.

The sooner we start dreaming big, the sooner the nightmare can stop.

A democratic alliance to promote human rights

[The following was originally published on Democracy Without Borders]

Recently United States Secretary of State Mike Pompeo called for “a new alliance of democracies” aimed at confronting China. This put democratic globalists in a difficult position. If you want global democracy, then surely an alliance of democracies confronting the lone authoritarian superpower is a good thing? But US imperialism is also an obstacle to a fairer, more equal world order.

Democracy Without Borders has already published one blog about this by Sven Biscop which focuses on this second concern, asking (from an entirely eurocentric perspective) whether this would be an alliance “with the US” or “for the US?”. This is an entirely valid concern, but overall this response is inadequate.

Biscop compares the proposal to the “Coalition of the Willing”, which the US assembled to back it’s invasion of Iraq, outside UN auspices. But this coalition did not require its members to be democracies. The US was, as it usually is, happy to work with dictatorships. Biscop ignores this, and the broader hypocrisy of US foregn policy.

US officials only object to human rights abuses when it suits them, but for Biscop — and much of the global commentariat — it seems that this is too often. Fundamentally, they too support a foreign policy position which is human-rights-agnostic.

At one point Biscop says “China is an authoritarian state … The EU and the US have to speak up for human rights” but his resistance to authoritarianism lasts only one sentence, and is shrugged off in the next, saying “because China is a great power, Europe and America … have little leverage.”

According to this view, it seems, conflict must be avoided at all costs. Trade must be allowed to flow, presumably including goods made by forced labour in the Uiger concentration camps. To the extent his piece is an attack on Pomeo’s cynical proposal, it is correct. To the extent it is a defence of the status quo, and an argument for appeasing authoritarians, tolerating their brutal intolerance, it is profoundly wrong.

Neither Pompeo nor Biscop try to imagine how a genuine a democratic alliance might function. But we can.

First, stop helping dictators

The very first step would not be to challenge, but merely to stop helping, authoritarian oppressors. Many dictatorships depend on the backing of established democracies to gain and maintain power.

For example in 2013 the US could have backed the elected government of Egypt and prevented the coup which brought the military strongman Abdel Fatah el-Sisi to power. The US supplies vital training and equipment to the Egyptian military, worth over a billion a year, as well as priceless geo-political support. It can not be seen as neutral. Looking for a reliable partner who would not have to justify their foreign policy posture to the Egyptian population, they chose the military strongman over the democratically elected president.

Unfortunately this move, overseen by the supposedly liberal President Barack Obama, is typical of US foreign policy, which goes to great efforts to subvert democracy and install, maintain and preserve dictatorships across the world.

Other elected governments overthrown by the United States or with its unambiguous assistance since the end of the Second World War include such as in Iran (1953), Guatemala (1954), Congo (1960), Brazil (1964), Greece (1967), or Chile (1973).

This is only a partial list, containing some of the most unambiguous historic cases, where unclassified documents show the US was actively working against foreign governments whose electoral legitimacy was clear. Many murkier cases exist, where the legitimacy of the government removed is more questionable, or the US role is less well documented — though it may be confirmed in the future by subsequent declassifications of relevant documents.

The tendency is for the US to back the right against the left which creates an environment where right wing coups can assume US support and diplomatic cover.

Hence the US (and its developed democratic allies) also bear a significant degree of responsibility for the fate of the Honduran government of President Manuel Zelaya, removed from power in 2009 with, at minimum, US acquiescence, the extremely questionable impeachment of Brazillian president Dilma Rousseff in 2016, and the fall of Bolivian government of Evo Morales, who resigned in 2019 following demands by the military (with whom the US has significant leverage through training and equipment supply).

As an absolutely prerequisite for the establishment of a credible democratic alliance, this behaviour must stop. The US must adopt, in word and in deed, something like the “progressive baseline” of democracy and human rights promotion proposed by Congresswoman Ilhan Omar.

Should this occur space would begin to be cleared for a grand democratic alliance to form.

Where to start?

An existing alliance like NATO could make membership conditional on meeting democratic and human rights standards (which would entail, for a start, expelling Turkey) and then expand to include any nation that met those democratic standards (as proposed by the Campaign for a World Democratic Security Community). Or the anti-Huawei “D10” recently proposed by Prime Minister Boris Johnson, of the UK as a way for democratic countries to counter China’s edge in 5G technology (and therefore telecom-espionage), might form the kernel. There are also diplomatic efforts like the Community of Democracies and the Streit Council which explicitly aims for the creation of an “international order of, by and for the people”. Both of these efforts emerge from eastern Europe in the immediate post-soviet era, and perhaps are tainted by an implicit eurocentrism, and an aftertaste of NATO triumphalism. The CoD’s website boasts of US secretary of state Madeleine Albright’s involvement in the Community of Democracies, as if this were an uncontroversially good thing, as if she were not famous for saying that the death of half a million Iraqi children was “worth it”, while defending US enforce sanctions on that country.

One initiative that actively seeks to leave this baggage behind, and rescue democracy from the wreckage of US foreign policy is the “Human Union” proposed by Australian activist Lyndon Storey, which calls for a new alliance, and stresses that it need not be western led. Japan, Uruguay and Botswana, for example, could form a loose union that would grow in membership and degree of integration until it became a global union of democratic states. Big, powerful western democracies like the US and UK could still join, but as equals, and on terms set by this broader community (including abandoning their authoritarian allies). The exact nature of this integration should not be laid out in advance, but would be negotiated between the parties along the way, as would the precise preconditions for entry — but the goal should unambiguously be the exclusion of authoritarian human rights abusers.

Whatever the origin of the organisation, it should focus on a long term goal of promoting a global political system based on democracy and human rights, rather than just reacting to the threat posed by one authoritarian actor, such as China.

An economic community of democracies

This alliance could form an economic community, where democracies closing ranks, granting each other preferential market access, and excluding authoritarian nations. The OECD could conceivably form the basis for this, if it became more aggressive in its promotion of democratic values, and helped establish preferential trade access between its members. Part of this reorientation as a bulwark against authoritarianism could be the inclusion of Taiwan.

Contrary to what some may say, such a strategy is extremely viable. In terms of population, democracies make up just less than half of the world. According to the Economist Intelligence Unit, full democracies make up 4.5%, flawed democracies (a category which, since 2016 includes the United States) makes up 43.2%. Hybrid regimes make up 16.7% and authoritarian regimes make up 35.6%.

In terms of economic power, though, measured here through by the IMF, the democracies clearly have the upperhand.

This is based on nominal GDP, which measures economies in terms of international dollars. It is thus the correct measure when it comes to international heft, but often in these discussions Purchasing Power Parity is used. This is either a result of ignorance, or a way of overstating Chinese power, understating our capacity -and therefore obligation- to act. In nominal terms the United Statesof America controls 24.5% of World Product. The EU controls 21.4%. The People’s Republic of China controls 16.2%.

Yet China alone is responsible for 61.9% of the economic activity in non-democratic states. Whereas the US only, represents 33.8% of the collective GDP of the democracies.

Democracies are not only stronger, their power is more evenly spread. Should the economic battle lines be drawn, there is no one country the democratic camp would rely on to the extent which the non democracies would rely on China.

We could do it, in other words, without the US. Maybe, if they won’t stop backing military juntas, we should.

Even without this superpower, the democratic nations have substantial leverage, and could use that — rather than military force or covert subterfuge — to promote human rights and democracy worldwide, culminating eventually in a democratic world order. There is no need for violence, and nothing stopping this values driven world order from emerging except a lack of political will.